By Patrick Werr – Reuters –

Egypt faces an increasingly tough task raising cash for foreign debt repayments after external borrowing quadrupled over the past eight years to help fund a new capital, build infrastructure, buy weapons and support an overvalued currenc.

Few of its grand projects are generating additional hard currency inflows, while foreign investors have added to its woes by snubbing Egypt and other emerging markets since the start of the Ukraine war and as global borrowing costs have climbed.

The government says it will meet repayments, but it has not delivered on long-promised structural changes to its economy and its bid to raise cash by selling state holdings has failed to offload any major assets for foreign currency for nearly a year.

“I think the biggest problem right now is that no one is seeing enough reform,” said Monica Malik at Abu Dhabi-based bank ADCB. “Egypt is waiting for capital flows, and no one I speak to is ready to put that in again until they see the reform.”

Investors have long pushed for a more flexible currency. But Egypt’s pound has not moved against the dollar for three months despite a pledge to the International Monetary Fund to free it up under a $3 billion financial package agreed in December.

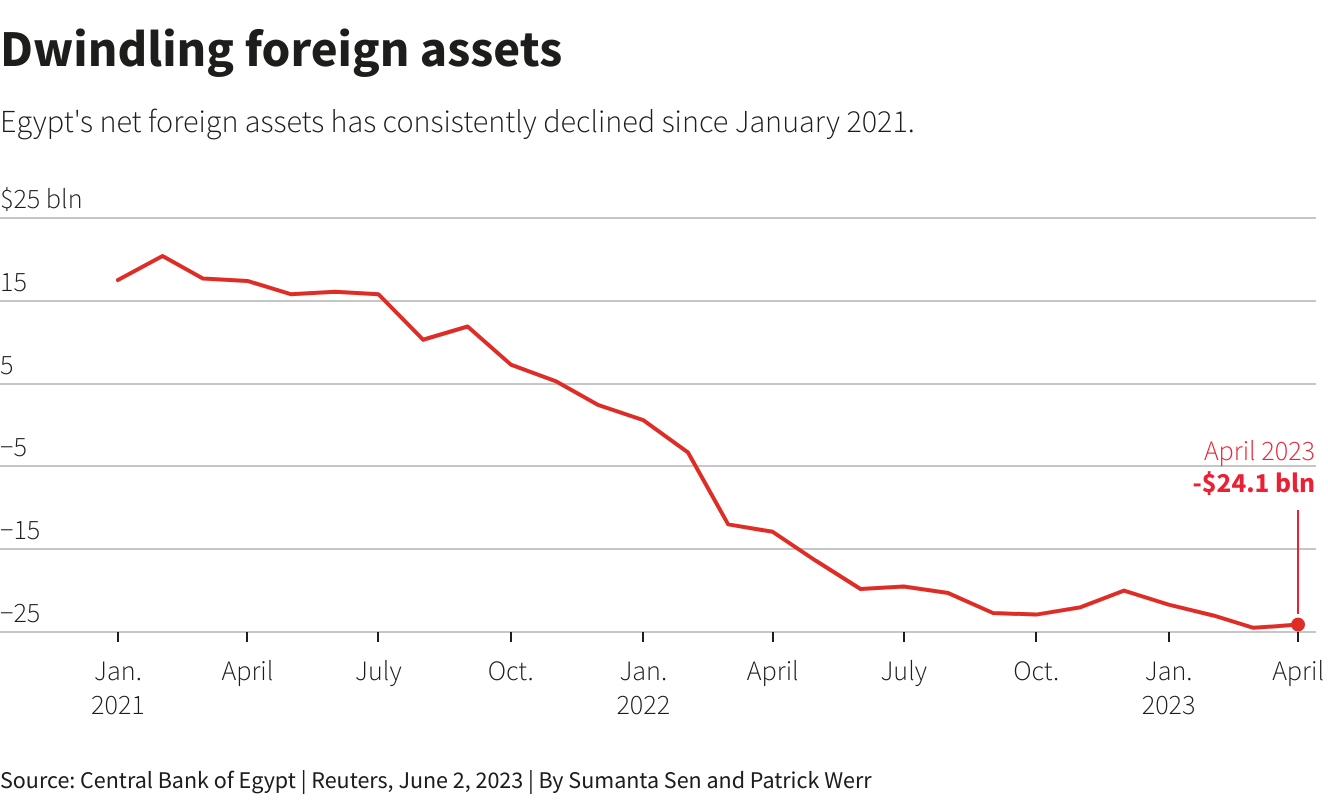

Amid a foreign currency crunch, Egypt has drawn down net foreign assets in the banking system by more than $40 billion in two years, partly used to prop up the pound.

Prime Minister Moustafa Madbouly has, meanwhile, sought to reassure investors about the state’s finances. “I affirm that the Egyptian state has not failed and will not fail to pay any of its international obligations,” he said in April.

Egypt said it will meet foreign liabilities and raise funds by selling assets, including $2 billion by the end of June.

The Finance Ministry did not respond to a request for comment for this article.

FINDING FOREIGN FUNDS

Two of Egypt’s main foreign currency streams, tourism and Suez Canal transit fees, have edged up. But a third, remittances from Egyptians working abroad, has dropped as more people repatriate funds by using the unofficial market, bankers say.

At the official rate, a dollar gets about 31 pounds, while at the unofficial rate it gets about 39 pounds.

The hard currency squeeze has raised concerns about Egypt’s ability to repay foreign debt. Since April, all three main credit agencies downgraded the outlook for Egyptian debt.

“Egypt’s large external debt maturity profile is becoming increasingly challenging,” Moody’s said.

Payments due include $2.49 billion in short-term debt in June, while in the second half of 2023 they include $3.86 billion in short-term borrowing and $11.38 billion in longer-term debt, central bank data showed last week.

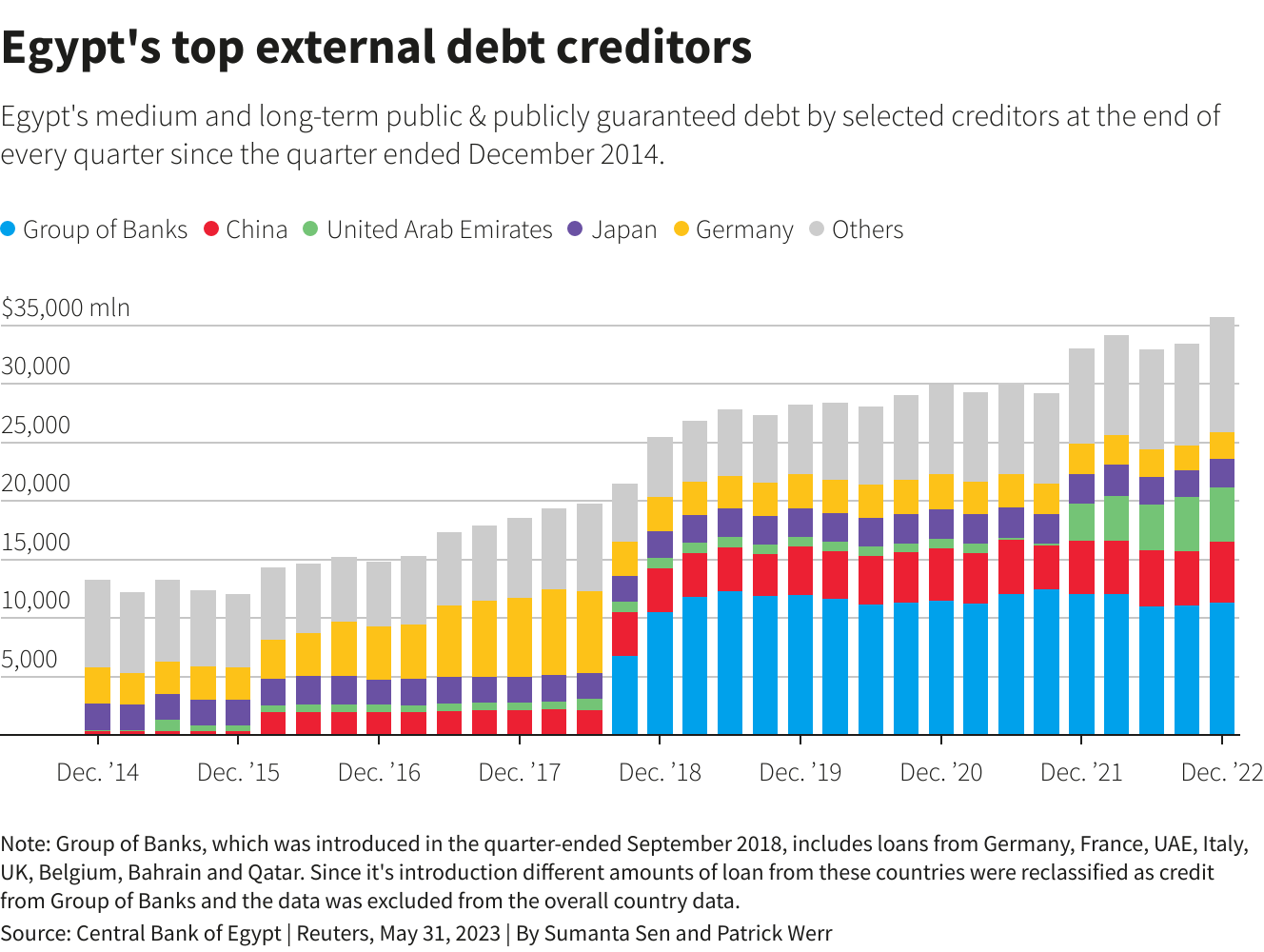

Some is owed to friendly lenders such Egypt’s Gulf allies. Based on past experience, they are likely to roll over nearly $30 billion they have deposited with Egypt’s central bank.

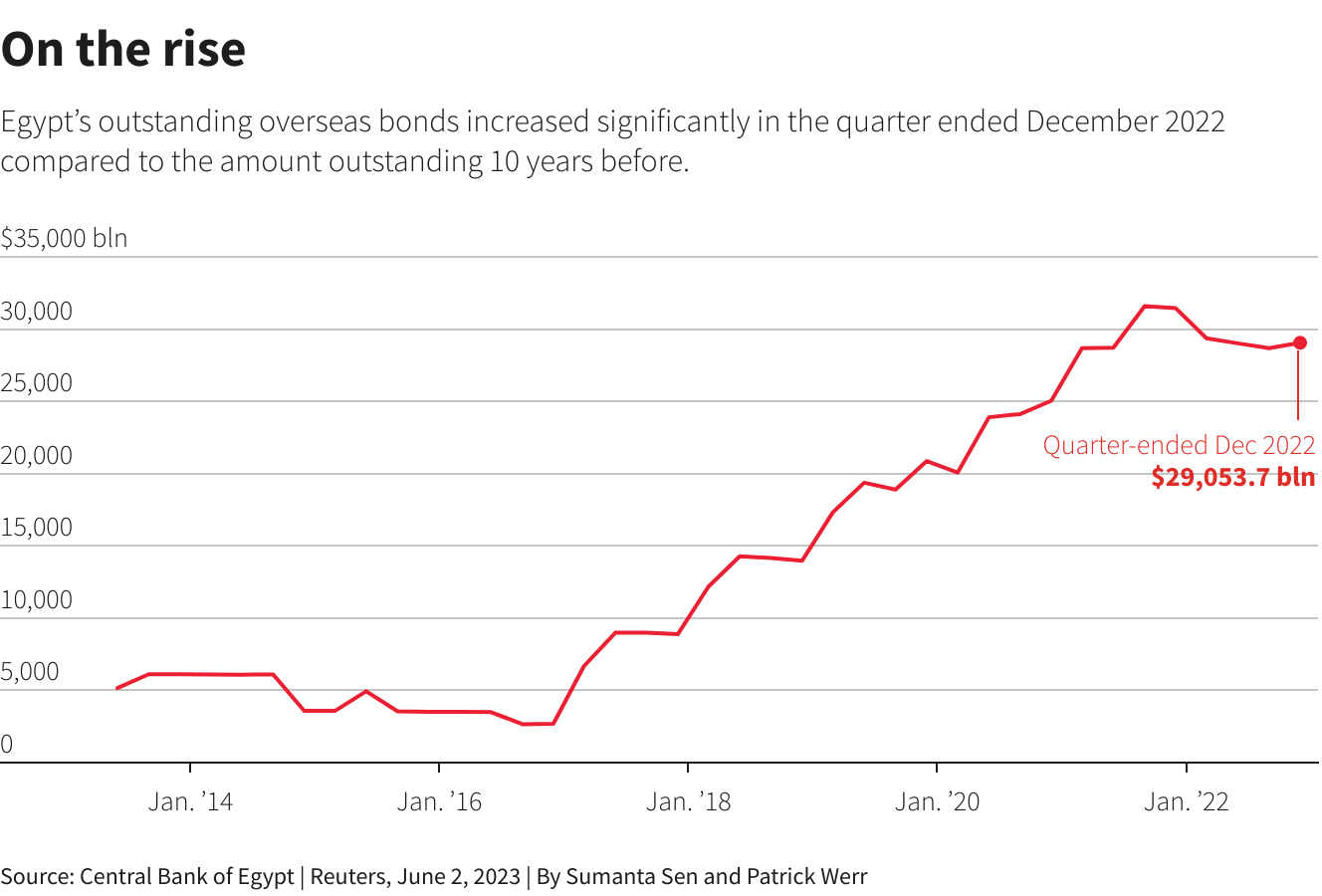

Other debt is owed to less forgiving lenders such as the IMF, to which it must pay $2.95 billion by the end of 2023, and foreign bond holders, who are due $1.58 billion. The repayment schedule is similarly onerous in subsequent years.

Those repayments to the IMF and foreign bond holders alone, worth about $4.5 billion, amount to more than half the annual $8 billion Egypt earns from the Suez Canal.

BORROWING BINGE

Egypt’s borrowing spree took off around a March 2015 economic conference, less than a year after general-turned-politican Abdel Fattah al-Sisi became president, when a series of megaprojects including a new capital city and three power plants were announced.

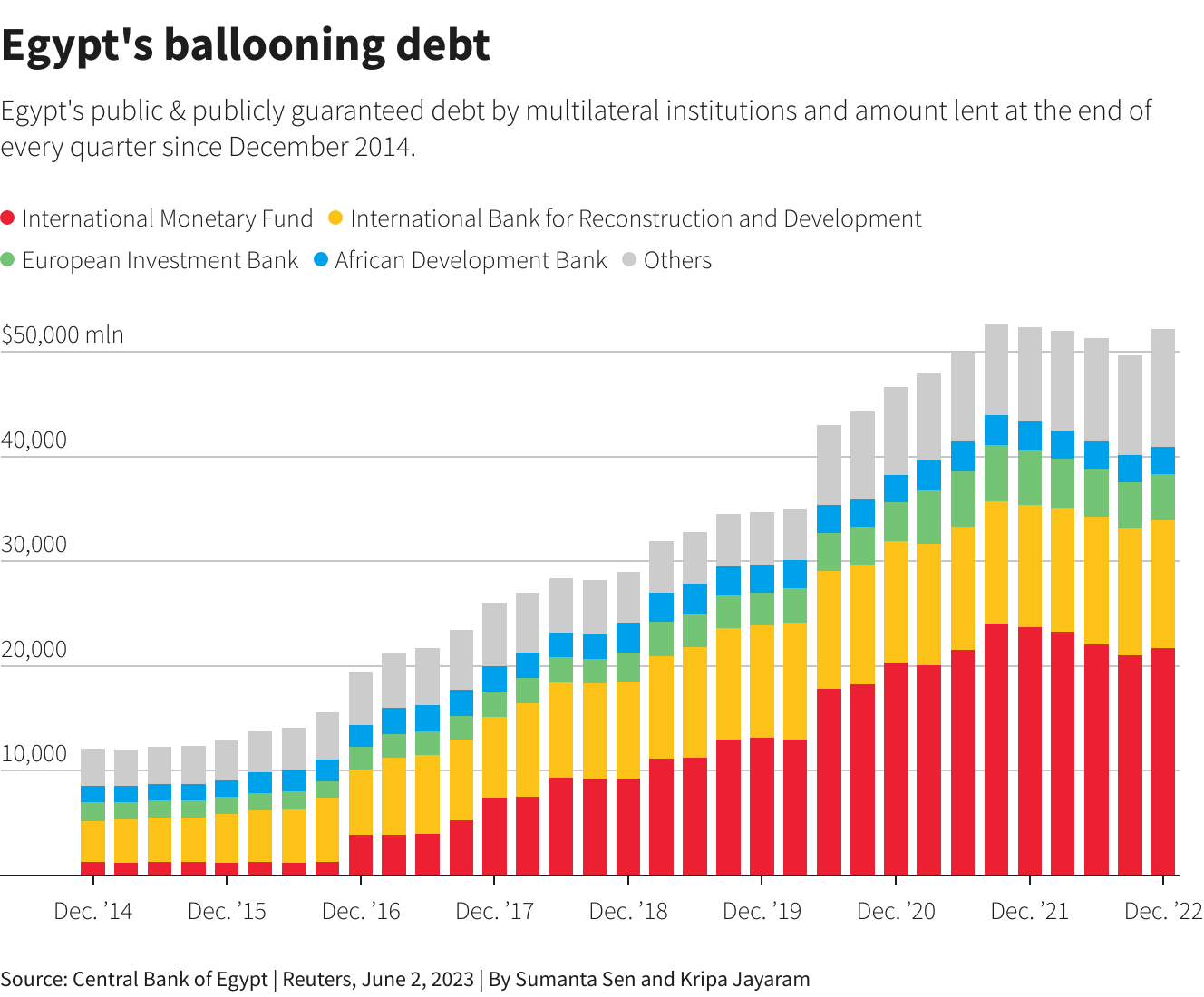

Reasssured by IMF deals in 2016 and 2020, multilateral lenders, foreign governments and institutional investors jumped on board.

Egypt, which hosted the COP27 climate summit last year, has also benefited from a wave of green financing.

Egypt’s external loans leapt to $162.9 billion by December 2022 from under $40 billion in 2015, central bank data showed. Borrowing in the last quarter of 2022 alone shot up by $8 billion.

“Egypt was the darling of the IMF and investors because of what it was doing on macro stabilisation,” said Farouk Soussa of Goldman Sachs.

“But the growth was too high, fuelled by borrowed money in a perverse circular logic; and the investment it fuelled has not provided the return hoped for in terms of enhancing ability to repay external debt,” he said.

Egypt, a nation of 105 million people that is one of the world’s biggest wheat importers and which also relies on imports of other basic foods and fuel, has spent much of the borrowed cash on projects that will not quickly generate the foreign currency it needs, economists say.

The projects include a new capital that will cost $58 billion to build east of Cairo, a $25 billion nuclear power plant on the Mediterranean coast and 2,000 km (1,250 miles) of high-speed rail network, the world’s sixth largest, that the presidency said will eventually cost $23 billion.

Between 2015 and 2019, Egypt became the world’s third largest arms importer, placing at least 54 weapons orders, the Stockholm International Peace Research Institute (SIPRI) says.

_____________________

Reuters Graphics Reuters Graphics

Reporting by Patrick Werr; Graphics by Sumanta Sen; Editing by Aidan Lewis and Edmund Blair

Photo: Vehicles drive on a road next to the construction site of the Iconic Tower skyscraper in the Central Business District (CBD), which is being built by China State Construction Engineering Corp (CSCEC) in the New Administrative Capital (NAC) east of Cairo, Egypt January 15, 2023. REUTERS/Amr Abdallah Dalsh/File Photo

{kind=link}