By The Wall Street Journal –

Weighed down by one of the world’s highest levels of foreign debt, Egypt faced a potential default if it didn’t begin making financial reforms..

Egypt struck a deal with the International Monetary Fund to extend the country an $8 billion loan, hours after allowing its currency to float freely and raising interest rates in a surprise bid to win back foreign investors as its economy comes under pressure from the war in Gaza.

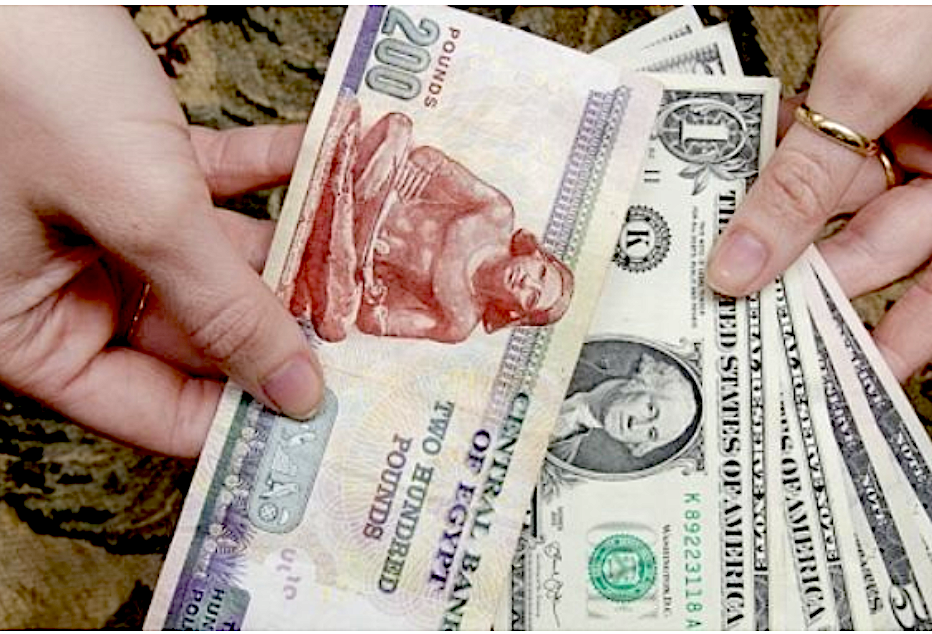

The Egyptian pound lost about 38% of its value against the U.S. dollar after the currency announcement, despite the Central Bank of Egypt raising key interest rates. The pound last traded at 49 pounds to one U.S. dollar, from about 30 the previous day.

The agreement marks a substantial step up from the $3 billion loan the IMF had been discussing with Cairo previously, signaling the organization’s willingness to help prop up the country’s economy.

Egypt’s currency announcement and rate move were part of a broader effort by authorities to attract foreign capital amid waning investor confidence and to stabilize a struggling domestic economy as the war in Gaza poses challenges to the government in Cairo.

Egypt has been playing a major role in cease-fire negotiations between Israel and Hamas and has sought to prevent a wider spillover of the conflict. But its ailing economy has come under renewed pressure. Weighed down by one of the world’s highest levels of foreign debt, Egypt faced a potential default if it didn’t begin making financial reforms that would attract investors and satisfy its international benefactors.

The war has raised diplomatic and political tensions across the Middle East and its economic impact has been felt in Europe and, to a lesser extent, the U.S. and Asia. Israel’s economy contracted sharply late last year as consumers cut spending in reaction to the uncertainty. The conflict has disrupted trade flows and briefly shut down production lines as far as Germany.

When Yemen’s Houthi forces began targeting vessels in the Red Sea in what they say is a response to Israel’s war in Gaza, many shipping operators rerouted their vessels, avoiding the Suez Canal linking Asia to the Mediterranean, reducing Egypt’s revenue from transit fees. Egyptian authorities also face a potential influx of tens of thousands of Palestinians trying to flee fighting between Israel and Hamas.

President Abdel Fattah Al Sisi, who was re-elected for a third presidential term in December, had resisted letting the pound drop dramatically as he sought to stabilize prices and keep political dissent in check, analysts said. Before Wednesday’s move, the pound had already lost about half its value since March 2022, pushing inflation to staggering levels and sending many Egyptian families into poverty.

Egyptian authorities, however, were under pressure to let the currency float freely, as a way to restore investor confidence. Egypt’s richer Gulf neighbors, which had propped up Egypt’s finances, have been reluctant in the past year to pump more capital into the country without reassurances on how the Egyptian pound would trade.

IMF discussions with Egypt over a loan have lasted for months, with officials pushing for Cairo to let its currency float freely in markets.

With the currency still under pressure and trading much lower in the black market, investors had for months been expecting the central bank to allow another sharp devaluation. Still, the announcement of a complete free float—and its timing on Wednesday—was a surprise.

In the short term, the sharp fall in the pound’s exchange rate could exacerbate inflation by making imports more expensive, resulting in additional hardship for most Egyptians, although many businesses had already been factoring in the move. Inflation eased to 29.8% in January, after reaching around 33.8% in December.

Many Egyptians have had to cut back on eating meat and some have blamed authorities for higher prices. “When the government floats the pound, it harms us even more,” said Alaa El-Sabea, a father of two young children in Cairo who has skipped his own lunch and dinner to save money. “The most important thing is to make sure my children eat.”

The IMF in October agreed to lend Egypt $3 billion, although it has delayed incoming tranches amid ongoing discussions about reforms that authorities were willing to commit to. The new deal Wednesday was announced in a press conference by Egyptian Prime Minister Mostafa Madbouly and IMF Egypt head Ivanna Vladkova Hollar, according to Egyptian state media.

“This will go a step further in restoring confidence in Egypt’s economy and perhaps giving Egypt easier access to private capital,” said Timothy Kaldas, an Egypt analyst at the Tahrir Institute for Middle East Policy.

“This only holds if authorities stop wasteful spending and commit to serious reform,” he said.

The Egyptian central bank said its sole objective now would be to rein in inflation, which it will aim to keep within a range between 5% and 9%. It raised its overnight deposit rate to 27.25% from 21.25%, having already raised rates by 2 percentage points last month.

“The announced measures have been adopted as part of a set of comprehensive economic reforms in coordination with the government, and backed by the steadfast support of multilateral and bilateral partners,” the central bank said.

Countries in the Middle East, as well as the U.S.—which regards Egypt as an ally in the region and provides it with more than $1 billion in military aid each year—have an incentive to help keep the Egyptian economy stable as the war in Gaza threatens to turn into a regional conflict.

The United Arab Emirates, along with Saudi Arabia, had grown increasingly reluctant to provide financial bailouts for Egypt, however, as they had done in the past. The Wall Street Journal reported last year that Gulf countries not only brought up Egypt’s management of the currency but also insisted it appoint new officials to run the economy.

Abu Dhabi-based investment firm ADQ last month agreed to invest $35 billion in megaprojects in Egypt, including on its north coast, contingent on authorities letting the Egyptian pound float freely, said people familiar with the deal.

The Central Bank of Egypt didn’t respond to a request for comment.

Economists warned that on its own, letting the currency float will only go so far in restoring investor confidence, given the government’s high level of deficit spending and the Egyptian military’s increased role in the economy.

“It’s a good step, but it’s too late,” said Alia El-Mahdi, an economics professor at Cairo University. “Encouraging the Egyptian private sector instead of selling state assets is essential.”

Before the war in Gaza, Egypt’s economy was hard-hit by the conflict in Ukraine, which sent global food and commodities prices soaring. Egyptian authorities scrambled to source wheat that they had been buying from Russia and Ukraine.

________________________

By The Wall Street Journal –

Weighed down by one of the world’s highest levels of foreign debt, Egypt faced a potential default if it didn’t begin making financial reforms..

Egypt struck a deal with the International Monetary Fund to extend the country an $8 billion loan, hours after allowing its currency to float freely and raising interest rates in a surprise bid to win back foreign investors as its economy comes under pressure from the war in Gaza.

The Egyptian pound lost about 38% of its value against the U.S. dollar after the currency announcement, despite the Central Bank of Egypt raising key interest rates. The pound last traded at 49 pounds to one U.S. dollar, from about 30 the previous day.

The agreement marks a substantial step up from the $3 billion loan the IMF had been discussing with Cairo previously, signaling the organization’s willingness to help prop up the country’s economy.

Egypt’s currency announcement and rate move were part of a broader effort by authorities to attract foreign capital amid waning investor confidence and to stabilize a struggling domestic economy as the war in Gaza poses challenges to the government in Cairo.

Egypt has been playing a major role in cease-fire negotiations between Israel and Hamas and has sought to prevent a wider spillover of the conflict. But its ailing economy has come under renewed pressure. Weighed down by one of the world’s highest levels of foreign debt, Egypt faced a potential default if it didn’t begin making financial reforms that would attract investors and satisfy its international benefactors.

The war has raised diplomatic and political tensions across the Middle East and its economic impact has been felt in Europe and, to a lesser extent, the U.S. and Asia. Israel’s economy contracted sharply late last year as consumers cut spending in reaction to the uncertainty. The conflict has disrupted trade flows and briefly shut down production lines as far as Germany.

When Yemen’s Houthi forces began targeting vessels in the Red Sea in what they say is a response to Israel’s war in Gaza, many shipping operators rerouted their vessels, avoiding the Suez Canal linking Asia to the Mediterranean, reducing Egypt’s revenue from transit fees. Egyptian authorities also face a potential influx of tens of thousands of Palestinians trying to flee fighting between Israel and Hamas.

President Abdel Fattah Al Sisi, who was re-elected for a third presidential term in December, had resisted letting the pound drop dramatically as he sought to stabilize prices and keep political dissent in check, analysts said. Before Wednesday’s move, the pound had already lost about half its value since March 2022, pushing inflation to staggering levels and sending many Egyptian families into poverty.

Egyptian authorities, however, were under pressure to let the currency float freely, as a way to restore investor confidence. Egypt’s richer Gulf neighbors, which had propped up Egypt’s finances, have been reluctant in the past year to pump more capital into the country without reassurances on how the Egyptian pound would trade.

IMF discussions with Egypt over a loan have lasted for months, with officials pushing for Cairo to let its currency float freely in markets.

With the currency still under pressure and trading much lower in the black market, investors had for months been expecting the central bank to allow another sharp devaluation. Still, the announcement of a complete free float—and its timing on Wednesday—was a surprise.

In the short term, the sharp fall in the pound’s exchange rate could exacerbate inflation by making imports more expensive, resulting in additional hardship for most Egyptians, although many businesses had already been factoring in the move. Inflation eased to 29.8% in January, after reaching around 33.8% in December.

Many Egyptians have had to cut back on eating meat and some have blamed authorities for higher prices. “When the government floats the pound, it harms us even more,” said Alaa El-Sabea, a father of two young children in Cairo who has skipped his own lunch and dinner to save money. “The most important thing is to make sure my children eat.”

The IMF in October agreed to lend Egypt $3 billion, although it has delayed incoming tranches amid ongoing discussions about reforms that authorities were willing to commit to. The new deal Wednesday was announced in a press conference by Egyptian Prime Minister Mostafa Madbouly and IMF Egypt head Ivanna Vladkova Hollar, according to Egyptian state media.

“This will go a step further in restoring confidence in Egypt’s economy and perhaps giving Egypt easier access to private capital,” said Timothy Kaldas, an Egypt analyst at the Tahrir Institute for Middle East Policy.

“This only holds if authorities stop wasteful spending and commit to serious reform,” he said.

The Egyptian central bank said its sole objective now would be to rein in inflation, which it will aim to keep within a range between 5% and 9%. It raised its overnight deposit rate to 27.25% from 21.25%, having already raised rates by 2 percentage points last month.

“The announced measures have been adopted as part of a set of comprehensive economic reforms in coordination with the government, and backed by the steadfast support of multilateral and bilateral partners,” the central bank said.

Countries in the Middle East, as well as the U.S.—which regards Egypt as an ally in the region and provides it with more than $1 billion in military aid each year—have an incentive to help keep the Egyptian economy stable as the war in Gaza threatens to turn into a regional conflict.

The United Arab Emirates, along with Saudi Arabia, had grown increasingly reluctant to provide financial bailouts for Egypt, however, as they had done in the past. The Wall Street Journal reported last year that Gulf countries not only brought up Egypt’s management of the currency but also insisted it appoint new officials to run the economy.

Abu Dhabi-based investment firm ADQ last month agreed to invest $35 billion in megaprojects in Egypt, including on its north coast, contingent on authorities letting the Egyptian pound float freely, said people familiar with the deal.

The Central Bank of Egypt didn’t respond to a request for comment.

Economists warned that on its own, letting the currency float will only go so far in restoring investor confidence, given the government’s high level of deficit spending and the Egyptian military’s increased role in the economy.

“It’s a good step, but it’s too late,” said Alia El-Mahdi, an economics professor at Cairo University. “Encouraging the Egyptian private sector instead of selling state assets is essential.”

Before the war in Gaza, Egypt’s economy was hard-hit by the conflict in Ukraine, which sent global food and commodities prices soaring. Egyptian authorities scrambled to source wheat that they had been buying from Russia and Ukraine.

________________________

{kind=link}